Empowering Consumers: The Role of AI in Legal Defense

Learn how to defend against small claims debt lawsuits, avoid default judgments, understand your rights, and use AI tools to build a stronger defense.

Receiving a summons for a debt collection lawsuit can feel incredibly unsettling. Many people facing these situations, especially in small claims court, often feel overwhelmed and unsure how to proceed. This confusion frequently leads to default judgments, with studies showing that more than 70% of defendants who don’t respond end up losing their case without a fight.

This reality underscores a vital need for clear, accessible information and effective defense strategies. We understand the stress and uncertainty that comes with legal action. That’s why we’ve created this comprehensive guide.

Throughout this article, we will walk you through the essentials of small claims debt defense. We will cover everything from understanding the court process and filing your response to identifying common defenses and preparing your evidence. Crucially, we will also explore how new technologies, including AI consumer debt defense, are making it easier for individuals to navigate these legal challenges and protect their rights. Our goal is to empower you with the knowledge and tools to confidently defend yourself.

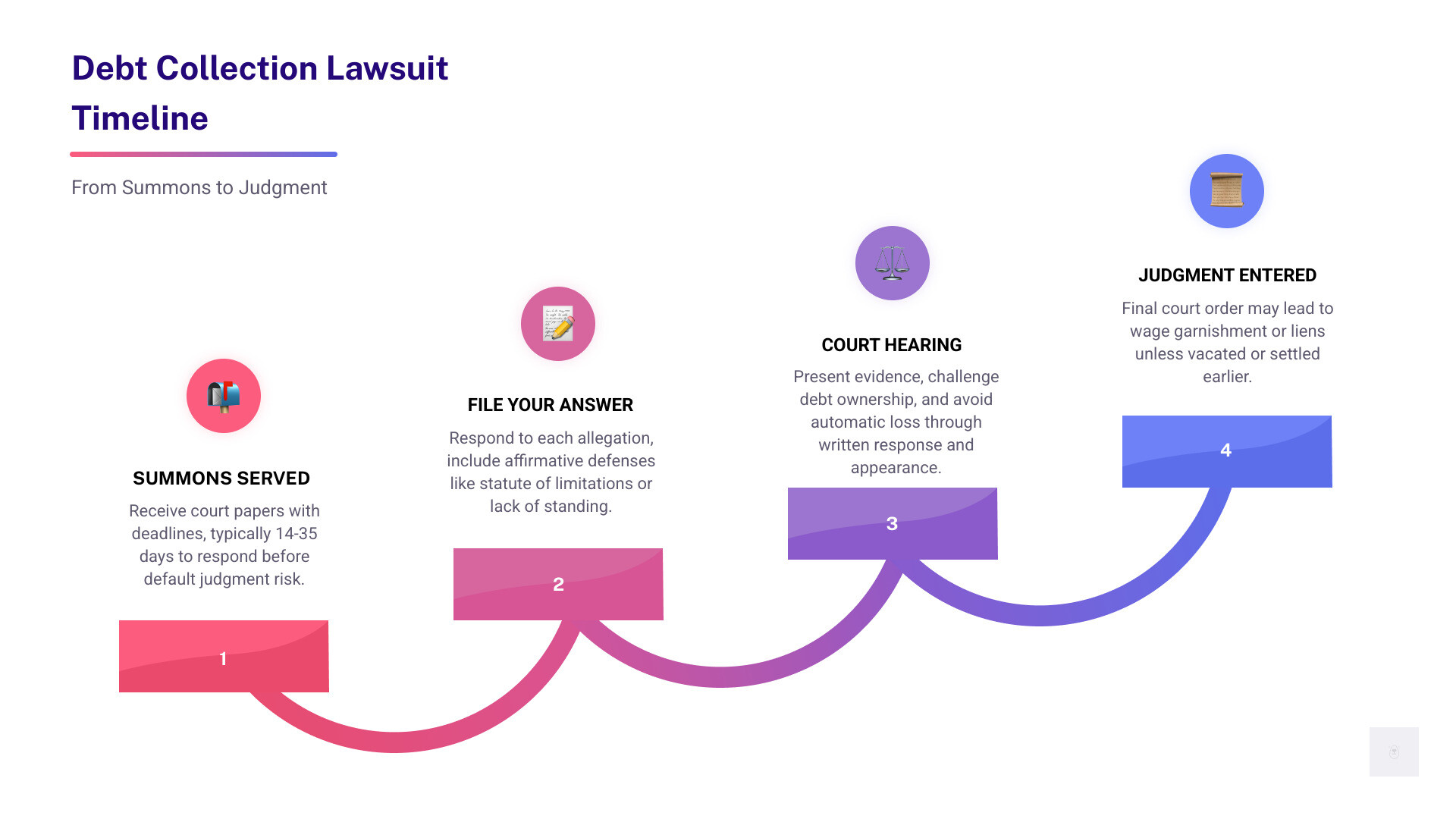

The moment you receive a summons for a small claims debt collection lawsuit, it’s natural to feel a surge of anxiety. However, this is a critical juncture where immediate, informed action can significantly alter the outcome. Ignoring the summons is the most common mistake, leading directly to a default judgment against you, which can then enable wage garnishment or asset seizure.

Small claims courts are designed to be less formal, making it easier for individuals to represent themselves without an attorney. These courts handle a significant portion of consumer debt collection cases, often involving amounts under $10,000. Debt collection lawsuits represent approximately 24% of all civil cases in state courts, highlighting the prevalence of these issues.

Your first step is to carefully review all the documents you’ve received. This includes the summons, which notifies you of the lawsuit, and the complaint, which outlines the plaintiff’s claims against you. Pay close attention to who is suing you (the plaintiff), the amount they claim you owe, and the deadline for your response. This response window is typically narrow, ranging from 14 to 35 days depending on your state’s rules. For instance, in Pennsylvania, you generally have 20 days, while in New Jersey, it’s 35 days. Missing this deadline is akin to forfeiting your right to defend yourself.

One common issue to be aware of is “sewer service,” where a plaintiff or process server claims to have served you but did not, or did so improperly. If you suspect improper service, this can be a valid defense to challenge the lawsuit. Additionally, verify the plaintiff’s legal standing – do they actually own the debt and have the right to sue you? Debt buyers, who purchase old debts for pennies on the dollar, often struggle to prove a clear chain of title.

Understanding these initial steps is paramount. For a comprehensive overview of how to manage these first crucial days, consider reviewing resources like “What to Do When Sued by a Debt Collector – Complete First Steps Guide” or “Sued for a Debt? Here’s Exactly What to Do in the First 7 Days” from KillDebt’s blog. These guides offer actionable advice for responding promptly and effectively.

Responding to a Summons and Complaint

Once you’ve absorbed the initial shock, your next crucial action is to prepare and file an Answer or response to the complaint. This formal document tells the court and the plaintiff your side of the story. While small claims courts often have simplified procedures, filing a proper Answer is usually required to avoid a default judgment.

The Answer typically involves responding to each numbered paragraph of the plaintiff’s complaint. You can admit, deny, or state that you lack sufficient knowledge to admit or deny each allegation. It’s crucial not to admit anything you’re unsure about. If a paragraph contains multiple claims, and you only agree with some, you should deny the entire paragraph or admit to the parts you agree with and deny the rest.

Beyond simply responding to the plaintiff’s claims, your Answer is where you raise “affirmative defenses.” These are reasons why, even if the plaintiff’s claims are true, they shouldn’t win the case. Common affirmative defenses in debt collection cases include:

- Statute of Limitations: The legal deadline for filing a lawsuit has passed.

- Identity Theft: The debt was incurred by someone else.

- Payment or Settlement: The debt has already been paid or settled.

- Lack of Standing: The plaintiff (especially a debt buyer) cannot prove they legally own the debt.

- Bankruptcy Discharge: The debt was discharged in a previous bankruptcy.

- FDCPA Violations: The debt collector violated your rights under the Fair Debt Collection Practices Act.

Many courts provide specific Answer forms for small claims cases, which can simplify this process. For example, Texas Justice Courts offer clear guidance on how to answer a debt collection case. Some states, like Michigan, even offer “Do-It-Yourself Civil Answer” tools.

Filing your Answer typically involves submitting it to the court clerk and then “serving” a copy to the plaintiff (or their attorney). This often requires sending it via certified mail with a return receipt requested to prove delivery. In some jurisdictions, you may also need to include a “Certificate of Service” with your filing. While filing fees for an Answer are often waived in debt collection cases, it’s always wise to check with your local court clerk. For a detailed walkthrough on drafting your response, KillDebt’s “How to Answer a Debt Summons” and “Sample Answer to Debt Collection Lawsuit” can be invaluable resources.

Avoiding the Default Judgment Trap

As highlighted by statistics, the risk of a default judgment is substantial, with default rates exceeding 70% when defendants fail to respond. A default judgment means the plaintiff automatically wins their case because you did not appear or file a timely response. This is a critical point: by simply failing to act, you lose your opportunity to present any defense, regardless of its merit.

Avoiding this trap is straightforward but requires diligence. The most important step is to file your Answer within the specified deadline. Even if you believe you owe the debt, responding allows you to negotiate a settlement, request proof of the debt, or explore payment options. Furthermore, merely appearing in court, even without a formal written answer in some small claims settings, can prevent a default judgment and give you a chance to explain your situation to the judge.

Once a default judgment is entered, it becomes a legally binding order. The plaintiff can then pursue various collection actions, such as wage garnishment, bank account levies, or property liens, depending on your state’s laws. While it may be possible to file a motion to vacate or reopen a default judgment, this is a complex legal process that requires demonstrating a valid reason for your failure to respond (e.g., improper service, excusable neglect) and a meritorious defense. It’s far simpler and more effective to respond proactively.

If you’re unsure about the process, many courts offer self-help centers or online resources to guide you. For example, the Nebraska Judicial Branch provides specific information for small claims court defendants. Your written response and appearance in court are your primary defenses against an automatic loss.

The Evolution of Legal Tech and Consumer Defense

The legal landscape, particularly for consumer debt defense, is undergoing a significant transformation, driven largely by advancements in legal technology. This evolution is crucial because it addresses a long-standing issue known as the “justice gap”—the disparity between the legal needs of low-income individuals and the resources available to meet those needs. For many pro se litigants (those representing themselves), navigating the complexities of the legal system, especially in small claims debt defense, has been an overwhelming and often losing battle.

Traditionally, defending a debt collection lawsuit required either hiring an attorney, which is often cost-prohibitive for individuals already struggling with debt, or attempting to navigate arcane legal procedures alone. This often led to the high default judgment rates we still observe. However, the rise of legal tech, particularly in the realm of document automation and AI-powered tools, is democratizing access to effective legal defense. These tools are designed to simplify complex legal processes, making them more accessible and understandable for everyday consumers.

The core idea is to empower individuals with the information and tools they need to stand up for their rights, even without a lawyer. This includes automated platforms that can help draft legal documents, track deadlines, and even offer strategic advice based on jurisdictional rules and common defenses.

How Legal Tech and Consumer Defense Tools Prevent Default Judgments

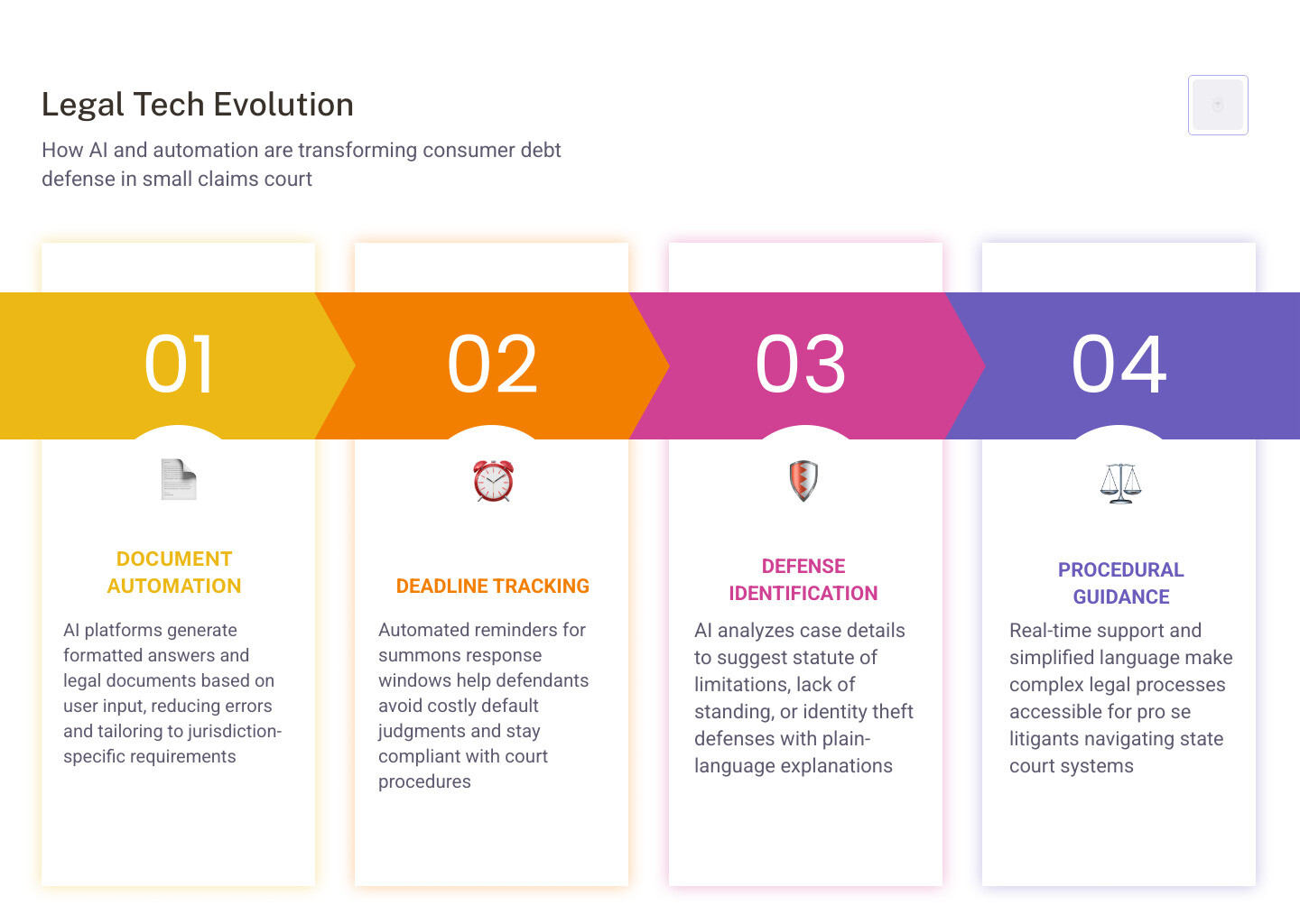

Legal technology plays a pivotal role in preventing default judgments by providing accessible, user-friendly solutions that guide defendants through the legal process. These tools, often leveraging artificial intelligence and automation, offer several key benefits:

- Automated Document Drafting: One of the most significant hurdles for pro se litigants is preparing legal documents like the Answer. Legal tech platforms can guide users through a series of questions, then automatically generate a professionally formatted Answer tailored to their specific situation and jurisdiction. This significantly reduces the chances of errors or omissions that could jeopardize a case. For instance, services like KillDebt offer tools to help draft answers efficiently.

- Deadline Tracking and Reminders: Missing a deadline is a primary cause of default judgments. Legal tech applications can track crucial dates—like the response deadline for a summons—and send automated reminders, ensuring defendants submit their documents on time.

- Statutory Research and Defense Identification: AI-powered tools can analyze the details of a user’s case and suggest potential defenses, such as the statute of limitations, identity theft, or lack of standing. They can even provide simplified explanations of relevant laws and regulations, like the Fair Debt Collection Practices Act (FDCPA).

- Language Simplification: Legal jargon is a major barrier. Legal tech often translates complex legal terms into plain language, making the process less intimidating and more comprehensible for non-lawyers.

- Jurisdictional Rule Adaptation: Legal procedures vary significantly from state to state, and even from county to county. Advanced legal tech solutions can incorporate these specific jurisdictional rules, ensuring that the generated documents and advice are compliant with local court requirements.

By streamlining these processes, legal tech empowers individuals to confidently respond to lawsuits, file necessary documents, and understand their rights, dramatically increasing their chances of avoiding a default judgment.

The Future of Legal Tech and Consumer Defense in State Courts

Looking ahead to May 2026, the integration of legal tech into state court systems and consumer defense strategies is only set to deepen. We anticipate several key trends:

- Virtual Hearings and Remote Appearances: The shift towards virtual court proceedings, accelerated by recent global events, is becoming a permanent fixture. Legal tech will continue to facilitate remote appearances, enabling defendants to participate in hearings from anywhere, reducing barriers like travel and time off work. Many courts, including some in Florida, now routinely allow remote appearances.

- Enhanced Digital Evidence Management: As more evidence becomes digital (e.g., emails, text messages, online transaction records), legal tech will offer sophisticated tools for organizing, presenting, and authenticating digital evidence, making it easier for defendants to build a compelling case.

- Seamless E-Filing Integration: Most state courts are moving towards mandatory e-filing. Legal tech platforms will offer seamless integration with these systems, allowing users to file their documents electronically directly from the application, further simplifying the process.

- Real-time Procedural Guidance: Imagine a tool that provides real-time, step-by-step guidance during a court hearing or while preparing for one. Future legal tech could offer interactive checklists, prompts for what to say, and even AI-driven simulations to help defendants practice their presentation.

- Data-Driven Outcome Prediction: While not legal advice, advanced AI could analyze vast datasets of past small claims cases to offer defendants insights into the likely outcomes of their specific situation, helping them make more informed decisions about settlement or trial.

The overarching goal is to create a more equitable legal system where technology bridges the gap between legal complexity and individual understanding, ensuring that access to justice is not a privilege but a right.

Strategic Defenses in Small Claims Court

Successfully defending a small claims debt collection case hinges on understanding and strategically employing various legal defenses. It’s not enough to simply deny the debt; you must present a compelling reason why the plaintiff’s claim is invalid or unenforceable.

One of the most powerful defenses is the statute of limitations. This is a time limit within which a lawsuit must be filed. If the debt collector files suit after this period has expired, you can ask the court to dismiss the case. The statute of limitations varies by state and type of debt, typically ranging from 3 to 6 years. For example, in Massachusetts, it’s 6 years, while in Pennsylvania, it’s often 4 years for most debts. It’s crucial to check your state’s specific laws.

Another common defense, especially against debt buyers, revolves around the chain of title. When a debt is sold from the original creditor to a debt buyer, there must be a clear, unbroken chain of documentation proving the transfer of ownership. Debt buyers often purchase large portfolios of old debt with incomplete or missing documentation, making it difficult for them to prove they legally own the debt and have the right to sue you. This is often referred to as “lack of standing.” The burden of proof is on the plaintiff to demonstrate they own the debt, that you owe it, and that the amount is accurate. If they cannot provide this proof, their case can be dismissed.

Hearsay objections can also be relevant. Debt buyers often rely on business records from the original creditor, which can be challenged as hearsay if the debt buyer cannot provide a witness who can authenticate those records. This is a common weakness in debt buyer lawsuits.

Challenging Ownership and Accuracy

When a debt collector, particularly a debt buyer, sues you, their primary challenge is often proving they have the legal right to collect the debt and that the amount claimed is accurate. This is where a robust defense challenging ownership and accuracy becomes critical.

- Proof of Ownership (Chain of Title): The plaintiff must demonstrate a clear and unbroken “chain of title” from the original creditor to themselves. This typically involves presenting purchase agreements, bills of sale, and assignment documents for each transfer of the debt. If the debt has been sold multiple times, every transfer must be documented. Missing links in this chain mean the plaintiff cannot prove they own the debt, and therefore, lack the legal standing to sue you. You have the right to demand this proof.

- Original Contract/Agreement: The plaintiff should be able to produce the original credit agreement, loan application, or contract that established the debt. This document proves the terms of the agreement, including the interest rate, and that you are the party responsible for the debt.

- Account Stated vs. Open Account: Many debt collection lawsuits are filed as “account stated” or “open account” claims. These rely on the idea that you implicitly agreed to the balance by not disputing regular statements. However, if the plaintiff cannot produce the original agreement or detailed transaction history, these claims can be challenged.

- Accuracy of the Amount Owed: Debt collectors frequently add various fees, interest, and charges to the original debt, sometimes without proper justification or in excess of what is legally allowed. You have the right to request a detailed accounting of the amount owed, including the original principal, all interest charges, fees, and payments made. Verify the interest rates against your original agreement and state usury laws. Inaccurate balances can be a strong point of contention.

- Payment History: If you have made payments on the debt, ensure the plaintiff’s records accurately reflect them. Discrepancies can indicate errors or even fraudulent practices.

By meticulously scrutinizing the plaintiff’s documentation for these elements, you can often uncover weaknesses in their case, forcing them to either drop the lawsuit or settle for a significantly reduced amount. For more insights on what a debt collector must prove, KillDebt’s article “What Does a Debt Collector Have to Prove in Court?” offers valuable guidance.

Raising Affirmative Defenses and Counterclaims

Beyond challenging the plaintiff’s case, you can also assert your own affirmative defenses and, in some situations, file a counterclaim.

Affirmative Defenses: These are reasons why, even if the plaintiff’s claims are true, they should not win. Common examples include:

- Identity Theft: If the debt was incurred fraudulently by someone else, you are not liable. You may need to provide a police report or a fraud affidavit.

- Bankruptcy Discharge: If the debt was included and discharged in a previous bankruptcy proceeding, it’s illegal for the collector to sue you.

- Fair Debt Collection Practices Act (FDCPA) Violations: The FDCPA protects consumers from abusive, unfair, or deceptive debt collection practices. Examples include calling at inconvenient times, threatening illegal actions, or misrepresenting the debt. If a debt collector violated the FDCPA, you might have a defense and even grounds for a counterclaim.

- Lack of Contract/Mutual Agreement: If there was no valid contract or agreement for the debt, you might argue you are not obligated.

- Payment or Settlement: If you have proof the debt was paid or settled, this is a clear defense.

Counterclaims: In some instances, you might have a claim against the plaintiff. This is called a counterclaim. For example, if the debt collector violated the FDCPA, you could sue them for damages. Some states allow for statutory damages (e.g., up to $1,000 per violation) and even attorney’s fees. If the plaintiff has harassed you with frivolous lawsuits, you can alert the judge, and in some cases, this can lead to treble damages against the plaintiff.

Filing a counterclaim can turn the tables, putting the plaintiff on the defensive. However, counterclaims must be filed promptly, often within the same timeframe as your Answer. In many states, if you don’t file a counterclaim when you have the opportunity, you may lose the right to sue the plaintiff for that issue later. If your counterclaim exceeds the small claims court’s monetary limit, the entire case might be transferred to a higher court. The NYC Bar Association’s “Information for the Defendant” provides useful details on counterclaims.

Leveraging AI for Document Analysis and Evidence Preparation

Preparing for a small claims debt defense case involves meticulous document analysis and evidence preparation. This is often where individuals without legal training feel most overwhelmed. However, modern legal tech, particularly AI-powered tools, can significantly streamline this process, making it more manageable and effective.

The discovery phase, though often simplified in small claims, is where parties exchange information. This might involve:

- Interrogatories: Written questions that the other party must answer under oath.

- Requests for Production: Demands for specific documents, such as the original contract, account statements, and chain of title documents.

- Requests for Admission: Asking the other party to admit or deny certain facts.

AI tools can assist in drafting these requests, ensuring they are comprehensive and legally sound. They can also help you organize the documents you receive, creating a clear “chain of custody” for your evidence. Digital receipts, emails, and other electronic records are increasingly important, and AI can help categorize and present them effectively. While witness testimony remains crucial, strong documentary evidence forms the backbone of most successful defenses.

Analyzing Debt Buyer Documentation

Debt buyers often acquire thousands of accounts in bulk, sometimes for pennies on the dollar. This business model frequently leads to significant issues with documentation, which you can leverage in your defense. AI-powered document analysis tools are particularly effective here:

- Identifying Missing Links: As discussed, the chain of title is critical. AI can rapidly scan and compare multiple documents (purchase agreements, bills of sale) to identify any missing assignments or transfers, highlighting gaps that undermine the debt buyer’s claim of ownership.

- Detecting Robo-Signing: In the past, some debt buyers engaged in “robo-signing,” where employees signed affidavits without verifying the information. AI can analyze signatures and document patterns to flag potential instances of robo-signing, which can invalidate the plaintiff’s sworn statements.

- Spotting Inaccurate Balances: AI can cross-reference the plaintiff’s claimed balance with your own records (if available) and the original creditor’s statements to identify discrepancies in principal, interest, and fees. This helps you challenge the accuracy of the amount owed.

- Verifying Validation Notices: Under the FDCPA, debt collectors must send you a “validation notice” within five days of their initial communication, informing you of your right to dispute the debt. AI tools can help you determine if this notice was properly sent and if your subsequent requests for validation were adequately addressed. If not, this could be an FDCPA violation.

By using AI to dissect the often voluminous and disorganized documentation provided by debt buyers, you can quickly pinpoint weaknesses in their case, turning their evidentiary shortcomings into your strategic advantage.

Preparing for the Small Claims Hearing

The small claims hearing is your opportunity to present your defense to the judge or magistrate. Preparation is key, and AI-powered tools can support you in several ways:

- Organizing Evidence Binders: AI can help categorize and index all your documents—contracts, statements, proof of payments, FDCPA violation evidence, and any discovery responses—into a logical, easy-to-navigate binder. This ensures you can quickly access specific documents when presenting your case or responding to the judge’s questions.

- Structuring Oral Testimony: While AI cannot speak for you, it can help you structure your narrative. You can input your key points and evidence, and the AI can help you outline a clear, chronological presentation that highlights your defenses and supports your claims. Practicing your oral presentation in front of others is also highly recommended.

- Identifying Potential Expert Witnesses: Although less common in small claims, if your case involves complex issues (e.g., property damage valuation), AI could help identify the types of expert witnesses whose testimony might strengthen your case.

- Mediation and Settlement Negotiation: Many small claims courts offer mediation as a way to resolve disputes before trial. This is a process where a neutral third party helps you and the plaintiff negotiate a settlement. AI tools can help you analyze the strengths and weaknesses of your case, as well as the plaintiff’s, to formulate a strong negotiation strategy. This includes suggesting reasonable settlement figures based on typical outcomes for similar cases. Any settlement agreement should always be in writing and signed by both parties. If you believe you may lose, negotiating a settlement can be a favorable option. The Florida Bar’s “About Small Claims Collection Lawsuits” highlights the role of mediation.

By leveraging these tools, you can walk into your small claims hearing feeling more confident and prepared, ready to present a clear, evidence-backed defense.

Frequently Asked Questions about Legal Tech and Consumer Defense

What are the most effective defenses in a small claims debt case?

The most effective defenses often revolve around challenging the plaintiff’s legal standing and the validity of the debt. These include:

- Statute of Limitations: The time limit for suing on the debt has expired. This is a powerful defense that can lead to dismissal.

- Lack of Standing/Proof of Ownership: The plaintiff (especially a debt buyer) cannot prove they legally own the debt and have the right to sue you. They must show a clear chain of title.

- Identity Theft: The debt was incurred by someone else, not you.

- Proof of Payment/Settlement: You have evidence that the debt has already been paid or settled.

- Inaccuracy of Amount: The plaintiff’s claimed amount is incorrect due to errors in calculations, unauthorized fees, or missing payment records.

- Bankruptcy Discharge: The debt was discharged in a previous bankruptcy proceeding.

- FDCPA Violations: The debt collector violated your rights under the Fair Debt Collection Practices Act.

How does AI help a defendant who cannot afford a lawyer?

AI-powered legal tech significantly levels the playing field for pro se defendants by:

- Document Drafting: Automating the creation of legal documents like Answers, counterclaims, and discovery requests, ensuring they meet court requirements.

- Procedural Education: Providing clear, simplified explanations of court procedures, deadlines, and legal concepts, reducing confusion and intimidation.

- Evidence Organization: Helping defendants categorize, index, and prepare their evidence (digital and physical) for presentation in court.

- Cost Reduction: Offering affordable or free tools that perform tasks traditionally requiring expensive legal professionals, making defense accessible regardless of income.

- Strategic Guidance: Suggesting potential defenses based on case details and jurisdictional rules, empowering defendants to make informed decisions.

These tools bridge the “justice gap,” allowing individuals to effectively assert their rights even without a lawyer.

Can I use legal tech to negotiate a settlement before my court date?

Yes, legal tech can be a valuable asset in preparing for and conducting settlement negotiations. While AI cannot directly negotiate for you, it can:

- Analyze Case Strength: Help you understand the strengths and weaknesses of both your case and the plaintiff’s, providing a realistic assessment of potential outcomes.

- Identify Negotiation Points: Highlight areas where the plaintiff’s case is weak (e.g., missing documentation, expired statute of limitations), giving you leverage.

- Suggest Settlement Ranges: Based on data from similar cases, AI might suggest a reasonable percentage of the debt to offer in a lump-sum settlement or propose viable payment plan structures.

- Draft Settlement Agreements: Assist in drafting written settlement offers and ensuring that any final agreement includes clear terms, such as case dismissal, a release of claims, and confirmation that the debt will not be sold to another collector.

Negotiating a settlement before court can save time, reduce stress, and prevent a judgment from appearing on your public record. Always ensure any settlement is in writing and clearly states that the case will be dismissed upon fulfillment of the agreement.

Conclusion

The journey through a small claims debt collection lawsuit can be daunting, but it doesn’t have to be a solo struggle. By understanding the court process, acting swiftly, and leveraging the power of modern legal technology, consumers are increasingly empowered to defend their rights and achieve favorable outcomes. From immediate response strategies and challenging the plaintiff’s standing to raising affirmative defenses and preparing compelling evidence, every step you take is a move towards protecting your financial future.

As we look ahead to May 2026, the ongoing evolution of legal tech promises even greater accessibility and efficiency in the realm of small claims debt defense. These innovations are not just about winning cases; they are about fostering judicial efficiency, upholding consumer rights, and ultimately, ensuring that access to justice is a reality for everyone. By embracing these tools and knowledge, individuals can transform what was once an overwhelming legal challenge into an opportunity to assert control and secure a fair resolution.